Blockchain Technology has altered the way we interpret challenges. It has helped in a lot of ways. It has become obvious that there are worthy benefits of using blockchain technology in different industries. To prove its utility, it too has broken out from the limitations of specialist markets and entered the mainstream of company operations across a range of sectors.

It is now clear that the distributed digital database has benefits in terms of scalability, transparency, speed, and cost-effectiveness. The fact that blockchain technology still has a ways to go and that some of its supposed benefits can actually be problematic.

Advantages of Blockchain technology

Prior to digging deeper, keep these two points in mind.

- First, despite the fact that all blockchains are based on the same technology, but respond differently according to each sector’s unique needs. Smaller blockchains with fewer users are quicker and more affordable.

- Secondly, blockchain is an evolving distributed ledger system. The advantages it currently provides are just the tip of the iceberg. They’re only going to get bigger over time.

Related: What is Blockchain technology and how does it work?

1- Blockchain is distributed and decentralized.

Some believe that blockchain’s primary benefit is the fact that no bank, organization, or government has authority over it. Why?

Because in a blockchain network, users don’t need to understand or trust each other before joining. It provides a trustless environment with full security. There is no third party involved in it. With a distributed ledger, all participating members may trust that they are viewing the most up-to-date version of the data. If a member’s ledger has been compromised in any way, most other users in the network will not trust it.

A decentralized company model makes it more difficult for an individual or small group to unilaterally and unfairly alter the rules to their own benefit. To enforce it, we don’t need any third parties; instead, we use computer code that won’t let anything other than the specified outcome occur.

Enterprise Ethereum Alliance Director Dan Burnett

2-Blockchain enables digital Tokenization of physical assets.

Tokens are digital representations of real-world assets or services. Tokenization means turning an asset into a digital token that can be used on a blockchain platform.

Tokenization’s Advantages

Numerous advantages accrue to token holders, and they can be grouped into three broad categories:

- It increases market liquidity and makes it easier for investors to buy fine art and real estate, which are usually harder and take more time to sell traditionally.

- It facilitates business deals by cutting out middlemen in the market.

- Cryptocurrency token trading may occur 24/7

- It allows the investor to check the whole asset history present on the blockchain.

3-Blockchain is democratizing; anyone can use it.

As a public platform, blockchain technology allows users and organizations to rebuild their connections with one another. Further, it removes barriers to entry for people who otherwise wouldn’t be able to take part in some areas of business and industry, either due to a lack of resources or connections. We don’t usually witness such monopoly-busting strength in the conventional markets we’re used to. Anyone can join in at any time, as long as they follow the few simple rules for making transactions on the blockchain.

Fixing international currency exchange:

Millions of people may now be able to use the banking system because of this democratization.

Today, more developing nations are connected to the international banking system, yet there are still challenges with making international payments (Cross-border payments). We hope this blockchain will help us figure this out.

Devon Drew, Founder & CEO, DFD Partners A Data-Driven Distribution Platform

4-Blockchain technology is extremely fast and efficient.

Just like email replaced snail mail as the primary means of written communication, blockchain technology reduces the time it takes to complete financial transactions.

It also gets rid of mistakes made by people because of automation.

By eliminating the need for many middlemen and streamlining procedures, blockchain can reduce the time it takes to complete a transaction from hours or days to mere minutes or seconds. Primarily, a digital ledger expedites the process of doing anything. For example, as an alternative to reading and haggling over a legal document, a smart contract may contain all of the pertinent information.

In the future, speed will continue to be a huge blockchain benefit. Even if it’s not possible at the moment, envision a closing on a home purchase or sale taking place in under an hour, from offer to acceptance to transfer of money.

Enterprise Ethereum Alliance Director Dan Burnett

5-Blockchain system is very economical and cost-effective.

Now, businesses invest heavily in the upkeep of their present infrastructure. That’s why cutting expenses and putting the savings into new projects or enhancing existing ones is a priority.

Blockchain technology allows businesses to significantly reduce the expenses often spent when working with external vendors. Since blockchain has no inherent centralized player, no vendor fees are required. There is also less need for human intervention when a transaction is being validated, saving you even more time and money.

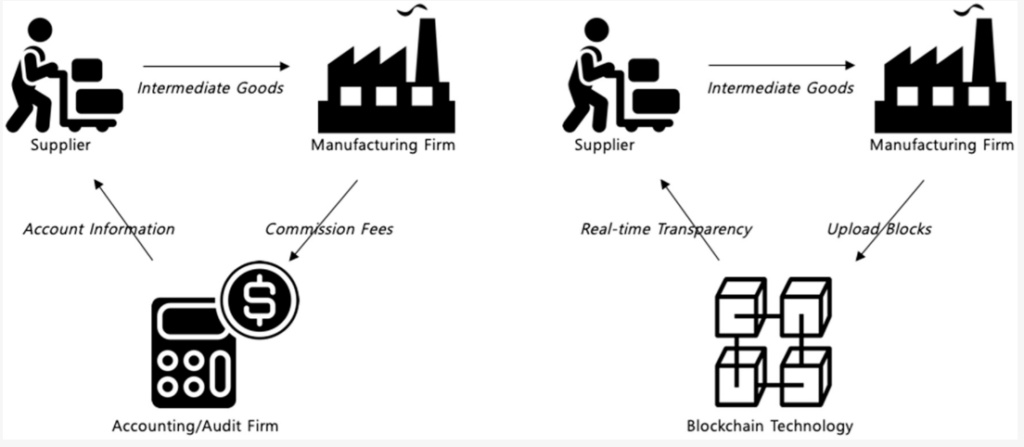

6-Block chain inspires trust and enhance traceability.

Blockchain technology allows businesses to concentrate on developing a supply chain that is compatible with both vendors and suppliers. Tracing products in the traditional supply chain is difficult, which can result in a number of issues such as counterfeiting, theft, and lost inventory.

Blockchain technology allows for greater visibility into the supply chain. It allows everyone involved in the supply chain to check the products for authenticity and make sure they aren’t being switched out or misappropriated. Blockchain traceability can also be implemented internally to ensure maximum benefits for businesses.

Example of enhanced traceability and trust

Smart contracts, which can be used to buy and sell items or carry out virtually any other form of agreement, are a prime illustration of this. Smart contracts are agreements between two parties that are recorded in a blockchain. When the conditions of the agreement are met, the transaction will be carried out immediately.

Once the smart contract has been recorded in the distributed ledger, it cannot be altered in any way. As a result, neither the buyer nor the seller may back out of the deal.

7-Blockchain technology ensures 100% transparency.

One of the major problems in the modern business world is a lack of transparency. More laws and regulations have been implemented by organizations in an effort to increase visibility. Nonetheless, centralization is the one factor that prevents any system from being completely open and honest.

By eliminating the need for central power, blockchain allows businesses to move toward a fully decentralized network that is more open to examination. In a blockchain system, every piece of data is publicly viewable. Whether or not the parties involved know each other’s identities, the terms of the transactions are still available. The potential for general welfare from this openness is enormous.

Blockchain will bring transparency to the government.

- If the government adopted a public blockchain system, citizens would have a better idea of where their tax dollars are going.

- Charities might utilize the blockchain to provide transparency to their donors about how their donations are being used.

8-Blockchain ledger technology guarantees a high level of security

When compared to older systems and ways of storing records, blockchain technology is incredibly safe. Any transaction that needs to be recorded forever must use the consensus method. In Blockchain, each transaction is encrypted with a hashing method and then appropriately linked to the one before it.

Every node in the network keeps a mirror copy of all transactions, which is an additional layer of protection. This ensures that no cyber criminal can ever change a transaction on the network since other nodes will always reject their request to write the transaction to the network.

As soon as information is recorded in a blockchain, it cannot be changed. Additionally, this is the optimal choice for data-heavy systems like citizen age databases.

Bottom Line: Great Benefits of using Blockchain Technology

In light of the above discussion, we can’t help but wonder about how much the world will improve once Blockchain is used universally.

With blockchain’s ongoing rapid rise, it will be used with the Internet of Things to facilitate confidence between companies, lessen the likelihood of manipulation, cut costs by eliminating middlemen, and speed up transactions from days to faster turnaround times.

Leave a Comment